On December 9, 2013, the food-away-from-home world was shocked to hear that Sysco and US Foods had agreed to “merge.” Although it was technically called a merger, it was clear that Sysco was buying US Foods. Behemoth #1 was buying Behemoth #2.

Fast forward nineteen months to June 29, 2015, and Sysco officially announces that it is terminating the US Foods merger agreement. Apparently, even in foodservice distribution, a monopoly is a monopoly, and the Federal Trade Commission (FTC) nixed the deal. With no one else big enough to buy US Foods, private equity firm owners KKR and CD&R made US Foods public on May 26, 2016.

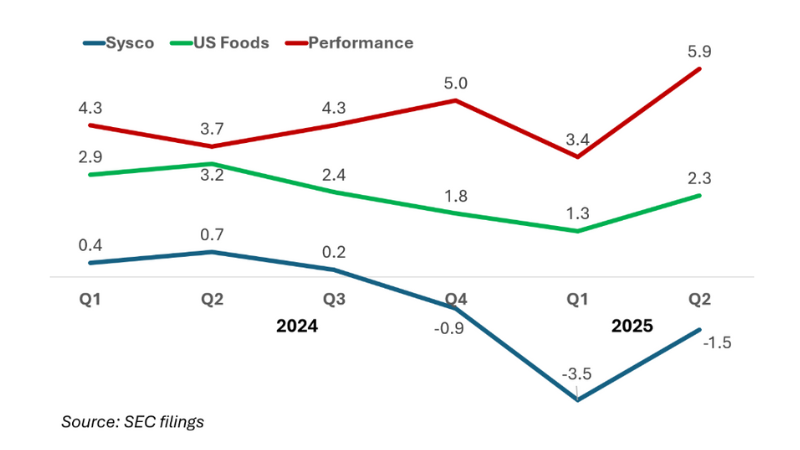

This history gives context to the current competitive environment between Sysco, US Foods, and Performance Foodservice, a division of Performance Food Group (PFG). The competition for cases is so fierce that acquisition is often seen as the only answer to get ahead. Specifically, the competition for local, or independent restaurant cases is at the heart of what drives profitability for these three companies. Over the last several quarters it’s clear that Sysco’s performance, in the local case volume KPI, continues to lag that of its two largest competitors.

YoY % Change in Local (Sysco) and Organic Independent Restaurant (USF and PFG) Case Volume (quarters are calendar based)

It's important to note that both Performance and US Foods’s case growth numbers are “organic,” while Sysco’s numbers include the impacts of the Edward Don acquisition. Sysco reported, “Our Edward Don acquisition, completed in the second quarter of fiscal 2024, positively impacted…local volumes by 1.6%.” Translated, this means local case volumes would have been down 1.4% without the Edward Don acquisition.

On the flip side, Performance Foodservice organic independent case growth continues to outperform both Sysco and US Foods by a substantial margin. Including the Cheney Brothers acquisition, independent case volume was up 20.4% in calendar Q2 and 5.9%, not including the acquisition.

When you look at the data, it’s hard not to assume that Sysco is losing market share in the most profitable segment of their business, local cases. Sysco would never confirm this, and we cannot be 100% confident that Sysco is losing market share to their main rivals, but the data does suggest this is happening.

The natural question that arises is why is this happening.

Sysco is the number one player in the market and should dominate a KPI that is price driven. If you ask Sysco CEO Kevin Hourican, he points to the compensation model of the Sysco Sales Consultant as the main cuprit. A new compensation model that was more bonus-based than salary-based appears to have backfired according to a recent article in the Wall Street Journal.

“’For Sysco, there’s a direct correlation between retaining employees and retaining customers,’ the CEO said. A restaurant’s rapport with its Sysco representative is usually just as strong as its relationship with Sysco itself, according to Hourican.” (WSJ. July 29, 2025)

If there is higher than expected turnover among sales representatives, you will see a decline in local case volume. Hourican now feels confident that the compensation problem is fixed and that “what was a headwind last year will be a tailwind this year.”

However, the headaches for Sysco keep on coming. On July 11, Bloomberg reported that US Foods is considering a takeover of PFG. On July 7, during a quarterly analyst call, David Flitman, CEO of US Foods, confirmed the report. “Our ask of PFG is simply to work together to further understand the merits and opportunities of a potential combination,” he said. If that deal happens, and is approved by the FTC, the pure foodservice business of US Foods, not including Vistar and Convenience businesses from PFG, becomes a $70.4B entity. Sysco’s U.S foodservice business is $57B.

The once unthinkable will happen: Behemoth #1 would step down to being Behemoth #2.

Manufacturers in the away-from-home food and beverage industry should keep apprised of the suddenly changing hierarchy among the “Big 3” broadline distributors. Putting all your cases into the basket of one of them could lead to volume declines that are out of your control. A less risky go-to-market strategy would be to diversify your cases across as many distributors as possible to mitigate volatility and risk.

A webinar with a full recap of calendar Q2 results from Sysco, US Foods, and Performance Foodservice is scheduled for Thursday August 28 at 11 AM CDT. Register here.

As Vice President of Industry Insights, Education & Research for IFMA The Food Away from Home Association, Charlie is a recognized expert in foodservice education and market strategy, with experience at NPD, Unilever, Sara Lee, and US Foods. He’s passionate about teaching others how to navigate the Food Away From Home industry through insights-driven marketing and strategy.